It’s a good time to invest in the fast-growing artificial intelligence (AI) industry. The market for AI is expected to surpass $184 billion this year, and forecast to reach more than $826 billion by 2030.

Among AI tech stocks, semiconductor firms Broadcom(NASDAQ: AVGO) and Advanced Micro Devices(NASDAQ: AMD) are two to consider investing in. The AI industry’s growth has led to outsized sales for both as customers flocked to their offerings.

Are You Missing The Morning Scoop?Breakfast News delivers it all in a quick, Foolish, and free daily newsletter. Sign Up For Free »

But if you had to choose between them, is one a better AI stock than the other? Let’s compare Broadcom and AMD to help you decide which is the better AI investment for the long run.

Broadcom is basking in the AI fervor, as sales expanded 47% year over year to $13.1 billion in its fiscal third quarter, ended Aug. 4. That’s an impressive increase, but 43% of the growth came from its acquisition of VMware, which closed last November.

VMware is famous for its virtualization software, which allows IT organizations to run multiple operating systems on a single server. But its private AI technology looks like a key strategic factor behind Broadcom’s acquisition.

Private AI shields a firm’s data from access by any AI system except those designated by the business. This is important because AI tech requires mountains of data, which is taken from various sources, including from businesses that have stored data in the cloud. Broadcom believes some companies don’t want their data shared with other businesses through AI, whether to protect intellectual property or to comply with legal requirements.

Broadcom’s private AI offering is built on the VMware Cloud Foundation (VCF) platform. VCF represented more than 80% of the VMware products booked in Q3. This illustrates strong customer demand for VCF and its ability to establish a private AI for businesses.

Broadcom also generates AI-related sales from an array of semiconductor products, including those for the computer networking, storage, and broadband industries. Its semiconductor solutions division contributed $7.3 billion of its $13.1 billion in Q3 revenue, a 5% year-over-year increase.

AMD’s strategy to capture AI market share is for its semiconductor products to concentrate on accelerated computing. This computing architecture processes data-intensive work separately from other computer tasks handled by a traditional CPU. Doing so allows complex software applications, such as AI, to operate faster and more efficiently.

AMD’s focus on accelerated computing has been the key to its success in the AI era. Big tech customers, such as Facebook parent Meta Platforms, are flocking to its products. For example, Meta purchased 1.5 million units of AMD’s EPYC computer processor for its cloud computing servers, which house AI systems.

This customer demand resulted in 18% year-over-year revenue growth to $6.8 billion in AMD’s fiscal third quarter, ended Sept. 28. Moreover, the company expects sales to accelerate in Q4, reaching about $7.5 billion, a 22% year-over-year increase.

AMD’s sales success has led to strong financials across the board. Its Q3 gross margin rose to 50% from 47% last year. This helped Q3 net income hit $771 million, a 158% jump up from the prior year. This, in turn, enabled diluted earnings per share (EPS) to increase to $0.47, a 161% year-over-year increase.

Both Broadcom and AMD possess AI strategies with the ability to capitalize on the growing AI market over the long term. This makes choosing only one of these AI stocks a challenge. So which wins?

One factor in Broadcom’s favor is that it offers a dividend, while AMD does not. Broadcom’s forward dividend yield is a solid 1.3% at the time of this writing.

However, excessive debt can put the dividend at risk. At the end of its fiscal Q3, Broadcom shouldered nearly $70 billion in debt. This resulted in more than $1 billion in Q3 interest payments, contributing to its net loss of $1.9 billion in the quarter.

Meanwhile, AMD’s debt at the end of its fiscal Q3 was a manageable $1.7 billion. With its Q3 cash and equivalents of $3.9 billion, AMD’s net debt was effectively zero.

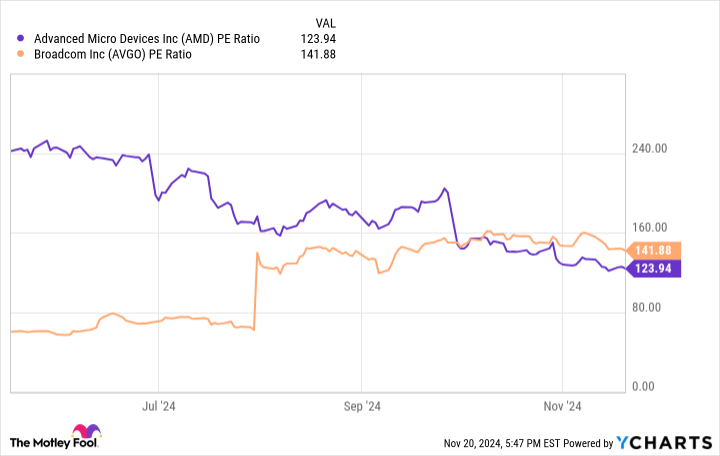

Another consideration is the price-to-earnings ratio (P/E ratio) for each company. This metric is a way to assess the relative value of a stock by telling you how much investors are willing to pay for every dollar of earnings.

Data by YCharts.

AMD’s P/E multiple was far higher than Broadcom’s earlier in 2024, but has come down recently. It’s below Broadcom’s at the time of this writing, suggesting AMD shares are now the better value.

Given these factors, as well as its success in the area of accelerated computing, right now AMD is the better AI stock to invest in the secular trend of artificial intelligence.

When our analyst team has a stock tip, it can pay to listen. After all, Stock Advisor’s total average return is 908% — a market-crushing outperformance compared to 174% for the S&P 500.*

They just revealed what they believe are the 10 best stocks for investors to buy right now… and Advanced Micro Devices made the list — but there are 9 other stocks you may be overlooking.

See the 10 stocks »

*Stock Advisor returns as of November 18, 2024

Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. Robert Izquierdo has positions in Advanced Micro Devices and Meta Platforms. The Motley Fool has positions in and recommends Advanced Micro Devices and Meta Platforms. The Motley Fool recommends Broadcom. The Motley Fool has a disclosure policy.

Better Artificial Intelligence Stock: Broadcom vs. AMD was originally published by The Motley Fool