With 2025 approaching, it’s time to start thinking about what stocks to add to your portfolio. While I’m a proponent of a well-diversified portfolio, I see a lot of potential in the tech realm right now, especially with how big artificial intelligence (AI) is becoming.

If you’re looking for a shopping list of stocks to buy in 2025, here’s a solid bunch of 10 to pick from.

If I had to buy just one stock from this list for 2025, I’d pick Taiwan Semiconductor Manufacturing (NYSE: TSM). Taiwan Semi is the world’s leading contract chip manufacturer and makes chips for nearly every company that produces anything related to high technology or AI.

Management expects AI-related revenue to triple this year, and there’s slim chance of that demand slowing down heading into 2025. With Wall Street expecting 25% revenue growth in 2025, I’d expect Taiwan Semi’s stock to excel next year.

Lastly, Taiwan Semi’s stock isn’t that expensive, trading for 22 times 2025 earnings. When you consider how important this company is, alongside its growth rate and reasonable price tag, it makes for a top stock to own in 2025.

ASML(NASDAQ: ASML) is similar to Taiwan Semi in that it’s an important supplier in the chip value stream. ASML makes lithography machines that nobody else in the world has the technology to make, giving it a technological monopoly.

However, this also causes problems as its machines are highly regulated, and most cannot be sold in China. As a result, management slashed 2025 revenue guidance, which caused the stock to tumble, and it is now down for the year.

This short-term weakness should be seen as a buying opportunity, as ASML’s tech is likely impossible to duplicate or catch up to, so it will be all right over the long term. Even with the guide down, Wall Street analysts still expect 15% growth next year, making ASML a great stock to buy now.

Meta Platforms (NASDAQ: META) is probably better known by its former name, Facebook. This social media giant generates a ton of revenue and profits from ad sales, but it’s also involved in the AI race.

Meta’s generative AI model, Llama, is the leading open-source AI model, making it a popular option for those who want visibility into what is actually happening behind the scenes. If Llama can become the top open-source AI model, it will collect vast amounts of information faster than other platforms that users must pay for, potentially opening up avenues for a paid version.

Still, that kind of success is a ways off, and right now, investors must base their analysis on the company’s ad division, which is doing incredibly well. Wall Street expects 21% revenue growth for 2024 and 15% for 2025. With strong growth in hand, Meta is set to have a strong 2025, with AI potentially another tailwind that has yet to meaningfully contribute to the business.

Alphabet (NASDAQ: GOOG)(NASDAQ: GOOGL) is another company heavily involved in the AI race. Its Google Gemini model is one of the leading options, and it can be further maximized by being deployed through Google Cloud, the company’s cloud computing wing.

Google Cloud grew by 35% in Q3 and is rapidly improving its operating margin. Although this segment makes up a fraction of Alphabet’s total revenue, it is one of the most exciting parts of its business and will drive it to market-beating growth.

With the stock trading recently for 25 times forward earnings, Alphabet is attractively priced compared to many of its big tech peers.

Amazon‘s (NASDAQ: AMZN) investment thesis is similar to Alphabet’s. It has a thriving primary business (in Amazon’s case, an e-commerce empire), but the cloud computing division is the primary reason to buy the stock.

Amazon Web Services (AWS) made up 17% of revenue in Q3, but its operating profits made up 60% of the company’s total. As a result, AWS heavily steers the company’s profit picture. With AWS growing at a healthy 19% clip in Q3 and no signs of AI-related growth slowing down, it’s primed to push Amazon higher in 2025.

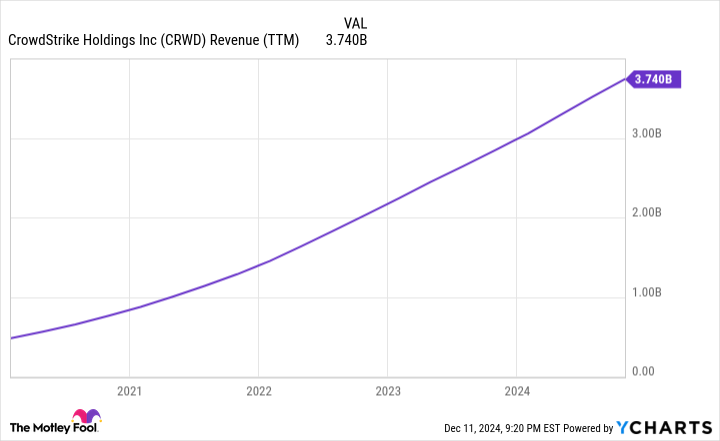

CrowdStrike (NASDAQ: CRWD) may be a bit of a controversial stock to include on this list. CrowdStrike is a cybersecurity company that gained a wider profile after a July 19 outage that crashed millions of devices. The effects of the crash are still being sorted, but that doesn’t mean the company isn’t strong. CEO George Kurtz has stated the company’s customer pipeline has returned to pre-incident levels, so the overall effect hasn’t been too bad.

In its last quarter (which encompasses a full quarter after the incident), annual recurring revenue (ARR) increased by 27% year over year to more than $4 billion, which is well on its way to achieving its goal of $10 billion in ARR.

CRWD Revenue (TTM) data by YCharts

CrowdStrike is a top cybersecurity provider; even a bit of a stumble wasn’t enough to derail the company. Although the stock is a bit pricey, I think it’s worth it for the growth that it’s putting up.

dLocal(NASDAQ: DLO) is a far more obscure company than any on this list. It provides a plug-in to anyone wanting to process payments in emerging market countries, unlocking access to parts of the world that wouldn’t make financial sense without dLocal’s services. Its client list includes giants like Amazon, Spotify Technology, and Shopify, demonstrating that its product fills an important niche.

dLocal is undergoing a transformation as new CEO Pedro Arnt takes over after a 12-year stint at MercadoLibre. He led an incredibly successful business there and has the blueprint to kick-start dLocal’s growth again.

With the stock trading for a mere 25 times forward earnings despite its profit margin being well off its previous highs, this stock has incredible value.

Speaking of incredible values, PayPal (NASDAQ: PYPL) is still a fairly cheap stock. The payment processing giant has gone through ups and downs but is currently on the rise, thanks to CEO Alex Chriss, who has been in the role for just over a year.

PayPal isn’t putting up the flashiest growth, with revenue rising 6% year over year in Q3 and earnings per share (EPS) rising about 6% as well. However, the company is diligently working to grow its business segments and using its cash to repurchase shares at a cheap price.

PYPL PE Ratio (Forward) data by YCharts

Although the stock isn’t as cheap as it used to be, trading at 19 times forward earnings, it’s still a pretty big bargain, especially considering that the S&P 500 trades at 22.5 times forward earnings. As a result, I think PayPal still has plenty of room for upside, and it could be the turnaround story of the year in 2025.

Next is MercadoLibre. The Latin American e-commerce and fintech giant has continuously posted incredible results year after year.

On a currency-neutral basis, MercadoLibre’s revenue rose more than 100% in Q3, showing its impressive platform. Although the company fell on a bit of a rough patch in Q3 as it dealt with some bad debt in its credit portfolio, that is a quarter-to-quarter problem that will pop up from time to time.

Although the stock isn’t cheap at 56 times forward earnings, its strong and sustainable growth justifies that price tag. As a result, I think it’s a phenomenal stock to buy in 2025.

Last but certainly not least is Nvidia (NASDAQ: NVDA). Nvidia has led the market each of the past two years, but I don’t expect it to do it again in 2025. However, with the largest AI players and cloud computing providers still building their computing power, Nvidia’s graphics processing unit (GPU) sales remain primed to benefit.

Furthermore, Nvidia’s Blackwell architecture, which offers massive performance gains over the current Hopper architecture, will reach full-scale production in 2025, further boosting Nvidia’s revenue.

Despite Nvidia’s massive growth over the past two years, Wall Street still expects its revenue to rise 51% next year. That’s enough to justify Nvidia’s price tag for me, and I think it’s a solid buy heading into 2025. Just don’t expect it to repeat 2023’s or 2024’s performance.

Before you buy stock in Taiwan Semiconductor Manufacturing, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Taiwan Semiconductor Manufacturing wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $841,692!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. TheStock Advisorservice has more than quadrupled the return of S&P 500 since 2002*.

See the 10 stocks »

*Stock Advisor returns as of December 9, 2024

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. Keithen Drury has positions in ASML, Alphabet, Amazon, CrowdStrike, DLocal, MercadoLibre, Meta Platforms, PayPal, Shopify, and Taiwan Semiconductor Manufacturing. The Motley Fool has positions in and recommends ASML, Alphabet, Amazon, CrowdStrike, MercadoLibre, Meta Platforms, Nvidia, PayPal, Shopify, Spotify Technology, and Taiwan Semiconductor Manufacturing. The Motley Fool recommends DLocal and recommends the following options: long January 2027 $42.50 calls on PayPal and short December 2024 $70 calls on PayPal. The Motley Fool has a disclosure policy.

Here Are My Top 10 Stocks for 2025 was originally published by The Motley Fool